Selecting comparable companies is an intricate aspect of valuation that requires a sophisticated blend of art and science. Practitioners must weigh a multitude of factors to ensure peers are appropriately chosen to reflect the intrinsic value of the company being analyzed. The selection process begins with defining the industry category, which often requires discerning judgment when dealing with companies that straddle multiple sectors.

The selection does not end with industry categorization; the financial criteria must be just as rigorous. Analysts frequently assess key financial metrics such as revenue size, market capitalization, EBITDA margins, and growth rates. While revenue may indicate the market scope the company operates within, EBITDA margins can shed light on operational efficiency and profitability comparability.

Geography also plays a crucial role as it can impact regulatory environments, tax considerations, and macroeconomic factors that differ from one region to another. Selecting comparable firms in similar geographic markets ensures that these extrinsic factors are neutralized.

An often-underestimated factor is the lifecycle stage of the companies in consideration. Firms in different lifecycle stages, whether startup, growth, maturity, or decline, exhibit markedly different risk profiles and financial performances. Selecting peers that align closely with the company's current lifecycle stage can provide more meaningful insights into valuation.

Trends and market conditions at the time of analysis significantly impact comparability. Economic cycles, interest rate environments, and industry-specific disruptions must be considered. Historical performance may offer context, but forward-looking considerations are more relevant in fast-evolving sectors where past data might not encapsulate current realities.

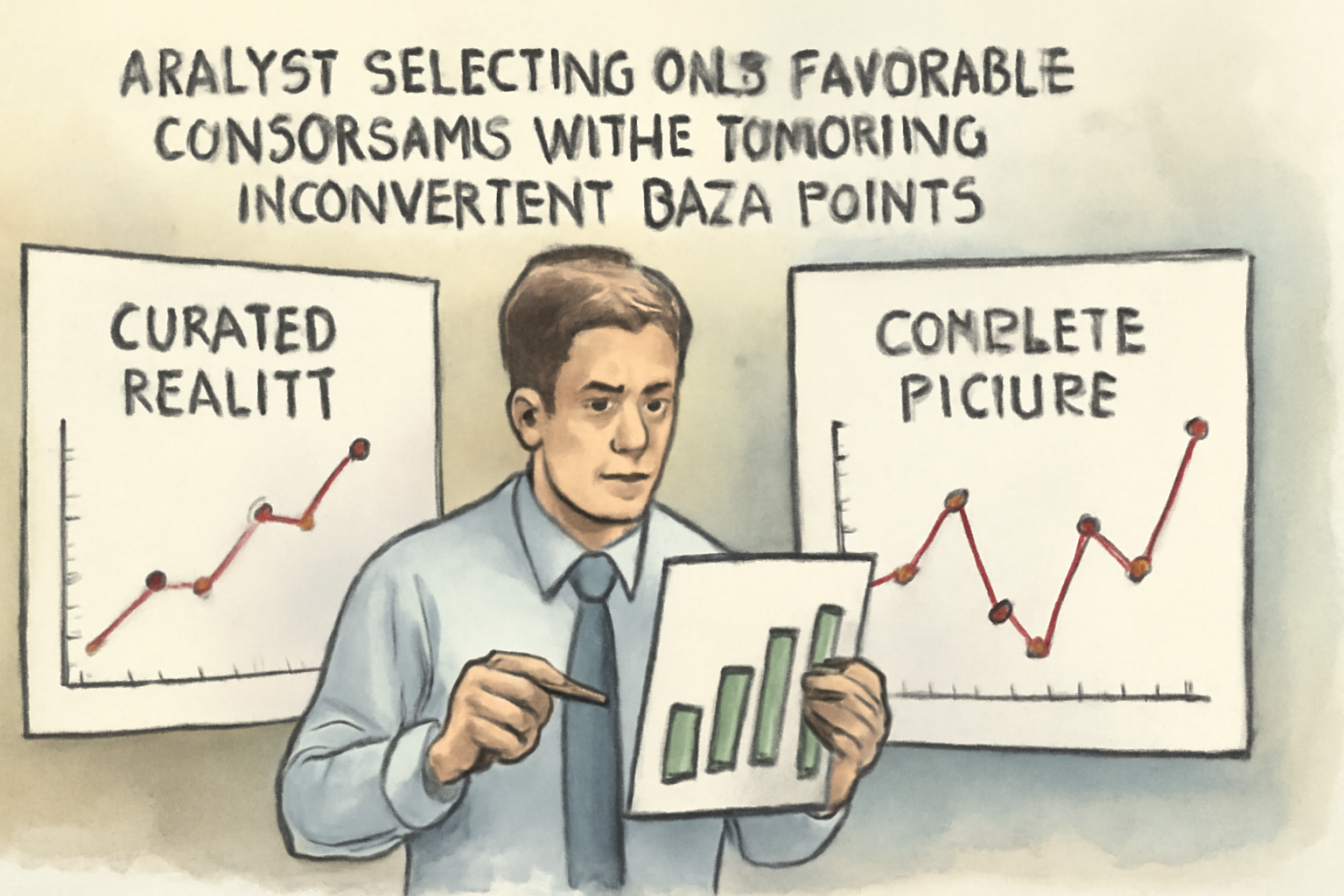

Furthermore, cherry-picking data is an inherent risk in selecting comparable companies. There exists the temptation to select peers that paint the subject company in an overly favorable light, leading to skewed valuations. Hence, maintaining objectivity and transparency in the selection criteria is paramount. Independent verification of data and adherence to a well-documented process can mitigate bias.

Finally, regulatory scrutiny around comparables warrants careful attention. Misleading representations of value can draw regulatory censure, making precision and rigor in the selection process not only a best practice but a necessity. Practitioners must document their methodologies meticulously to defend their analysis under inspection, ensuring compliance with relevant financial disclosure standards.